When President Roosevelt signed the GI Bill into law in 1944, he also approved provisions to begin low interest loans to Veterans looking to purchase their own homes, along with farming and business inventory. Soon, VA will guarantee its 20 millionth home loan, and the program is stronger than ever.

It’s not too hard to sell Veterans on the idea of a VA-backed home loan. As the only major loan type that doesn’t require a down payment, it also allows refinancing on existing loans, which was attractive to many Vets last year. Those who refinanced saved an average of $202 in 2012—a total of $300 million in savings.

Even in an unpredictable housing market, Veterans are finding their way to VA-backed loans. As the New York Times reports, VA-guaranty loans surged this past fiscal year:

Mortgages guaranteed by the Department of Veterans Affairs surged by 50 percent in the fiscal year ended Sept. 30, as tighter credit standards on conventional financing made these programs all the more attractive to current and former military members.

The department guaranteed almost 540,000 loans in fiscal year 2012, the most since 1994[…]

Since the loans are backed by the federal government, there’s no need for mortgage insurance, which can help Vets save even more. And if you’re a Veteran receiving disability payments, the funding fee, usually about three percent of the loan, is exempt.

Brandon Friedman, a Veteran of Iraq and Afghanistan, bought a house in the Washington, DC area a few years ago using a VA-backed loan, and his exemption from a funding fee saved him around $10,000.

“VA’s home loan program is one of the best benefits the government provides for Veterans, especially disabled Veterans,” he said. “It’d be great if more Vets knew about it.”

Check out our home loan resource page for more information, our frequently asked questions guide, and our eligibility page for more information. Andif you have any additional questions about the program, the Veterans Benefits Administration will be holding a live Twitter Town Hall tomorrow, October 18 at 3:30 PM EST. Follow @VAVetBenefits and use the hashtag #AskVA to ask your home loan question.

Topics in this story

More Stories

The findings of this new MVP study underscore the importance and positive impact of diverse representation in genetic research, paving the way for significant advances in health care tailored to Veteran population-specific needs.

VA reduces complexity for Veterans, beneficiaries, and caregivers signing in to VA.gov, VA’s official mobile app, and other VA online services while continuing to secure Veteran data.

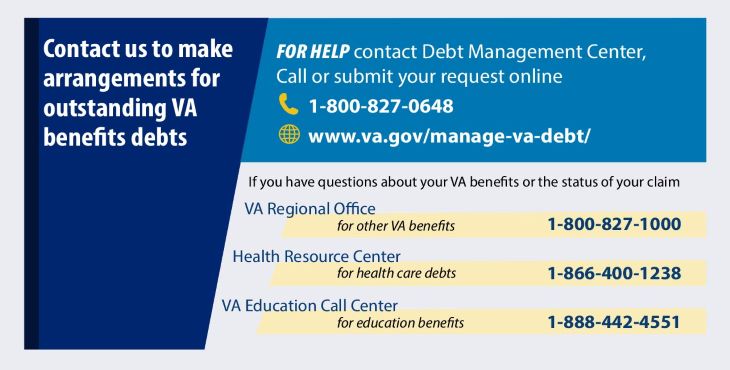

VA has resources available to ensure natural disasters do not make the already challenging situation of owing a VA debt worse. If you are experiencing financial hardship and are unable to repay your VA debt because of a natural disaster, relief options are available.

I purchase my house 14 months ago with my va loan, I did have a va inspection and private inspection. It was stated by seller and I was under impression the house was connected to city sewage. I recently found out the house has a septic tank and is not connected to city sewage, is there anything I can do, septic tank failed and Can’t be used properly. Where can I find legal support with the va.

Ricardo:

We recommend you contact your local office ( http://www.benefits.va.gov/homeloans/rlcweb.asp) to discuss your specific case. The representative will be able to access the appraisal report and see what the appriaser reported regarding city sewer or septic. A copy of that report should also have been given to you.

if i have a va loan thats backed by fed gov do i need home owners ins

Phil:

Thanks for your question. Yes: VA regs state that the holder (lender/servicer) shall require insurance policies to be procured and maintained in an amount sufficient to protect the security against the risks or hazards to which it may be subjected to the extent customary in the locality.

I am a veteran, recently got out of the Marine Corps a year an one month ago.. I have bad credit, applied for a home loan Literally less than 86,000$ an got declined…. Is their just no hope period for people like me?

Eric:

Yes, there is definitely hope because credit can be reestablished. Generally, credit is considered reestablished if satisfactory payments are made for 12 months after the date the last missed credit item is satisfied. You may want to call our offices and discuss your case in detail with a representative. They will have more tips to share: http://www.benefits.va.gov/homeloans/rlcweb.asp.

I am really disappoinnted with the VA loan. I am an IRAQI vet. Its was actually easier for me to get approve with Wells Fargo Bank than VA Loan. Thank you

I am 80% disable Veteran and unable to work since January/2012 because of my Service Connection and I tried and tried with the bank to get some kind of arrangement but they won’t answer my calls, I have an appeal with the BVA since June/2012 my claim start on 2001, and it look like nobody care. Help I look, help not answer. Anything else I can do so I won’t loose my house?

Juan:

Thank you for your question. I am so sorry to hear that you have been having these problems. Please call 1-877-827-3702 and speak with a VA representative who can discuss your options.

You might also find the information here useful: http://www.benefits.va.gov/homeloans/docs/foreclosure_avoidance_fact_sheet.pdf It lists some options in avoiding foreclosure.

Many soldiers and veterans returning from Iraq and. Afghanistan return to find bad credit – from debts they may not owe but weren’t in country to challenge, divorces affecting credit, etc. Attempting to use VA loans, they are told that VA requires a minimum credit score that they may not possess. My questions are:

1. Is this true? Does VA require a minimum credit score for one of their loans? If so, what is it, and why is this information not prominently available?

2. If not true, what does VA plan to do about this unscrupulous practice?

3. Perhaps more importantly, what is VA doing to help get veterans with bad credit but the ability to pay into homes? (Credit repair services, a list of lenders and their minimum scores, etc.) Is this issue even on VA’s radar?

4. Veterans are being told that if they are married, it is the lowest credit score (between them and their spouse) that will be used for the purposes of determining eligibility – not the veteran’s or the highest score. Why is this?

@Army:

VA does not require a minimum credit score. But, lenders who make the loans can impose requirements over and above our guidelines. Veterans are encouraged to check with more than one lender when shopping for a loan.

If a misleading ad does come to our attention, we will attempt to contact that lender to correct them. We also publish VA credit guidelines on the web: http://www.benefits.va.gov/warms/pam26_7.asp

The law requires a veteran to be a satisfactory credit risk before VA can guarantee the loan. But a veteran doesn’t have to have perfect credit. While VA doesn’t require credit scores, lenders use them. Generally, if there are 3 scores, lenders use the middle one. If married applicants, lenders usually take the middle score of both, then use the lower of those.

What is the minimum credit score required in order to obtain a VA loan?

Bonnie: VA does not require a minimum credit score. Lenders who make the loans can impose requirements over and above our guidelines and generally use credit scores. The minimum a lender may require can vary. We recommend you check out more than one lender before making your decision.

I already have the certificate telling me how much I am eligible for but now I don’t know what to do. Is there a special website or phone number to guide me thru the next steps? Thank You

Linda: We recommend you call and speak to a VA representative about the details of your prospective loan. Contact information can be found here: http://www.benefits.va.gov/homeloans/rlcweb.asp

You might also find this information helpful when planning your next steps: http://www.benefits.va.gov/homeloans/docs/vap_26-4_online_version.pdf

Are va home loans for veterans with a general under honerable conditions discharge?

John: A general under honorable discharge is accepted for Veterans who served on regular active duty (but not for Reserve or Guard). Try registering and applying for a Certificate of Eligibility at: http://www.ebenefits.va.gov or contact the eligibility center at 1-888-768-2132.

My wife bought a house using her VA loan. Can i use my VA loan on her house for home improvement?

Richard:

You could use your benefit for a VA cash-out refinance loan and use proceeds to make improvements. The key though will be the value of the property. That will determine how much equity you may be able to access.

I want to buy a home that costs only $10,000. I am unemployed, but with my disability, I could afford the mortgage for this home as the market is very low in the area for this home. I would even be able to pay the home loan off with my taxes. Then at least I would have the comfort of knowing I would always have a place to stay, if nothing else. So my question is, what do you do with a person with my criteria?

Mahogany:

It might be best for you to talk to a VA loan specialist to discuss this in more detail. Check the following link for local contact information: http://www.benefits.va.gov/homeloans/rlcweb.asp

Are there any out of pocket cost for VA Loan? if I get pre-approved and decide not to use the loan, can I refuse it or apply later?

Antonette:

Yes, there are closing costs associated with a VA guaranteed loan. The amounts can vary and can be negotiated with the seller.

Regarding pre-approval, lenders actually make the loan. If you are pre-approved by a lender but decide against using the benefit now you will be able to use the VA benefit again. Since the loan didn’t happen, you would not be using any of your VA entitlement.

I have a VA home loan. My loan was originally with Countrywide and when Bank of America bought them out it has been downhill ever since. I have had a decrease in income. Last year I had to report BOA to the OCC in order for them to stop giving me the run around and process my loan modification. It was still processed incorrectly. In April of this year I applied with a government funded program to get assistance with my mortgage. Six months later I was denied. I NEED TO KNOW what can be done at this point to save my home! HELP!!

B0FA IS UNDER COURT ORDER TO OFFER ASSISTANCE TO HOMEOWNERS AND THEY SENT OUT 250,000 LETTERS TO HOMEOWNERS AS A ONE SHOT DEAL. I YOU RECEIVED IT, YOU HAD TO REPLY TIMELY AND IF YOU LOST IT OR DISCARDED IT THEY WERE OFF THE HOOK.

BEST OF LUCK AND PEACE BE WITH YOU.

MS. BURRIS

Short Sale and Phantom Tax Debt Relief Overview

Lots of questions have arisen from people since President Bush signed into law the Mortgage Forgiveness Debt Relief Act of 2007, whereby in certain circumstances, a homeowner does not have to pay federal income tax on debt forgiven on a loan secured by a qualified principal residence via a short sale, foreclosure, deed in lieu, loan workout or short refinance where the loan amount was reduced and forgiven in order for the homeowner to keep the property.

It is somewhat confusing just reading a bill with only references to other sections of the law. Below is the text of Section 2 of H.R. 3648 that specifically pertains to mortgage forgiveness. To save you the hassle of cross-referencing all this, I have included the sections of the IRS Tax Code that were added to or modified as a result of Section 2 of H.R. 3648.

SECTION 1. SHORT TITLE.

This Act may be cited as the ‘‘Mortgage Forgiveness Debt Relief Act of 2007’’.

SECTION 2. DISCHARGES OF INDEBTEDNESS ON PRINCIPAL RESIDENCE EXCLUDED FROM GROSS INCOME.

(a) IN GENERAL. Paragraph (1) of section 108(a) of the Internal Revenue Code of 1986 is amended by striking ‘‘or’’ at the end of subparagraph (C), by striking the period at the end of subparagraph (D) and inserting ‘‘, or’’, and by inserting after subparagraph (D) the following new subparagraph: ‘‘(E) the indebtedness discharged is qualified principal residence indebtedness which is discharged before January 1, 2010.’’.

(b) SPECIAL RULES RELATING TO QUALIFIED PRINCIPAL RESIDENCE INDEBTEDNESS. Section 108 of such Code is amended by adding at the end the following new subsection:

‘‘(h) SPECIAL RULES RELATING TO QUALIFIED PRINCIPAL RESIDENCE INDEBTEDNESS.—

‘‘(1) BASIS REDUCTION.—The amount excluded from gross income by reason of subsection (a)(1)(E) shall be applied to reduce (but not below zero) the basis of the principal residence of the taxpayer.

‘‘(2) QUALIFIED PRINCIPAL RESIDENCE INDEBTEDNESS.—For purposes of this section, the term ‘qualified principal residence indebtedness’ means acquisition indebtedness (within the meaning of section 163(h)(3)(B), applied by substituting ‘$2,000,000 ($1,000,000’ for ‘$1,000,000 ($500,000’ in clause (ii) thereof) with respect to the principal residence of the taxpayer.

‘‘(3) EXCEPTION FOR CERTAIN DISCHARGES NOT RELATED TO TAXPAYER’S FINANCIAL CONDITION.—Subsection (a)(1)(E) shall not apply to the discharge of a loan if the discharge is on account of services performed for the lender or any other factor not directly related to a decline in the…

I just remarried and I am a 100% service connected disabled vet. I used my GI Bill to buy a house in Tennessee, but since sold it 25 years ago. I applied for a VA backed loan of $240,000 and was sent a letter from the VA saying that I was only eligible for some ludicris amout of $2600. Maybe a typo? Whiskey Tango Foxtrot!

You can’t buy an out house for that in Maryland. I commute just about everyday about 50 miles to and from the VA Hospital in Martinsburg and am currently sharing a house with my wife in her name. I have a Real Estate Broker who says I am eligible for $260,000. My Wife and I share an old house / School House built in 1880 and lacks many of the necessary essentials. We would like to move 25 miles closer to the Hospital for my benefit and enjoy having a bathroom on the same floor we sleep, central air, a garage would be the icing (no pun intended) on the cake. The interest rate is down to 4% and there is no better time to buy. We will rent out this old house to my Kids.

Charles:

If the previous loan is paid in full and you no longer own the property, you should be able to get full eligibility restored. Please contact the eligibility center to discuss: 1-888-768-2132.

More info: http://www.benefits.va.gov/homeloans/elig_center.asp

I have tried to refinance many times even tried to get a patriot loan express to start my wife her own business but here in wv no bank will do any type of va loan they always say the same thing there is a load of paperwork and it takes too long but i think what the problem is is that these greedy banks dont want to lose money on the interest rate they will lose plus if God forbid I did default they know I would have some help and rights and they dont want that. I have contacted the senator for wva with no help at all just wanted someone to know

Ricky:

Last year we guarantied over 500,000 loans and more than 40% of those were refinance loans. We’d recommend you compare options with a variety of different lenders.

Im a 64yr. old disabled Nan era Vet. Will my age be a factor.

Brad:

No. It’s actually against the law to discriminate on the basis of age!

I need to know if, as a surviving spouse, AND a veteran myself I can use my late husband’s VA eligibility. I owned a home ten years ago that was so badly damaged by a Section 8 tenant that I could not afford to repair it, and the home was surrendered to the lender in a “Deed in Lieu of Foreclosure” action that accompanied a Chapter 7 bankruptcy action in 2004.

My late husband left me over $150,000 in debt with accounts that I knew nothing about. Bankruptcy was my only option.

I did not know at the time that I could have applied to the VA to have the home repaired and made handicapped accessible to accommodate my handicap.

Ruth:

Typically, if you are a Veteran with home loan benefits entitlement, you can not also use the benefits as a surviving spouse. We’d recommend contacting your local loan center to talk to someone about your specific case and also about your questions on adaptive housing benefits: http://www.benefits.va.gov/homeloans/rlcweb.asp

I’m a Vietnam veteran and I’ve never used my benefits to buy a home, I had a conventional home loan and lost my home last year trying to get a modification. Can I get a home now using my vet benefits?

Melvin:

Because this is a complicated issue that may depend a lot on the details of your case, we’d recommend contacting your local loan center to speak directly with us. You can find the contact information here: http://www.benefits.va.gov/homeloans/rlcweb.asp

In most cases, VA treats foreclosure like a bankruptcy filing, meaning most applicants will have to wait for two years before applying for a new loan.

There is a limit of $417,000 on loans that can be guaranteed by the VA loan program. If the house you want to buy is more expensive, the difference must be made up with a down payment. Second loans for down payments must be at an interest rate equal to or less than the primary loan.

why cant the va back a loan on a class a rv if its going to be primary residence?????????

Jeff:

Unfortunately, we’re not authorized under the current law to guaranty loans on a RV.