The Consumer Finance Protection Bureau has some words for mortgage lenders looking to mislead Veterans.

In a press release today, CFPB put about 12 mortgage lenders on notice for potentially misleading advertisements targeting older folks and Veterans. Additionally, six companies are under investigation for potentially more serious violations.

CFPB identified a number of problems with mortgage advertisements, like inaccurate interest rates and misrepresentation of government affiliations.

From the release:

Today’s actions stem from a joint “sweep,” a review conducted by the CFPB and the FTC of about 800 randomly selected mortgage-related ads across the country, including ads for mortgage loans, refinancing, and reverse mortgages.

Holly Petraeus, CFPB’s Assistant Director of Service Member Affairs, adds today:

Some advertisers will use your military or veteran status as a way to approach you, promising special deals or implying VA approval. Others will use the lure of a “no-payment” reverse mortgage to troll for older Americans desperate to find a way to stay in their home when they can no longer afford a mortgage payment.

The bottom line? Work directly with your bank to ensure a VA-backed loan works for you. Check out our previous entries on home loans for more information: here, here, and here. And to receive updates from the watchdogs at CFPB, follow them on Facebook and Twitter.

Topics in this story

More Stories

The findings of this new MVP study underscore the importance and positive impact of diverse representation in genetic research, paving the way for significant advances in health care tailored to Veteran population-specific needs.

VA reduces complexity for Veterans, beneficiaries, and caregivers signing in to VA.gov, VA’s official mobile app, and other VA online services while continuing to secure Veteran data.

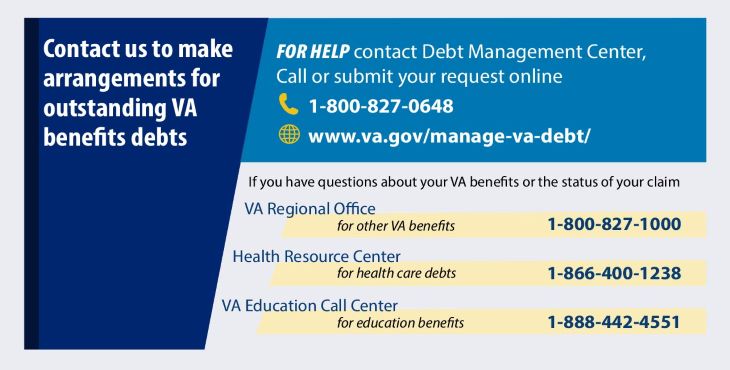

VA has resources available to ensure natural disasters do not make the already challenging situation of owing a VA debt worse. If you are experiencing financial hardship and are unable to repay your VA debt because of a natural disaster, relief options are available.

Yes, I had a refinance of Wells Fargo loan in Florida by M.I.C. in October 2002 and they almost immediately sold the loan to Washington Mutual.

Has anyone ever heard or used MIC Mortgage Investors Corp out of FL to refinance a VA loan? Any feedback would be welcome.

A Tease- I actual expect more from” Vantage Point” the publication of the VA. It seems they want to help veterans “(?) but have to be careful not to help them too much or they might damage the reputation of the predatory lenders. Better to let those veterans who were “marks” for those lenders are better served by the VA than the Veterans themselves. They sell out the veteran once more on the stone alter of business. Were in hopes that these businesses will perform correctly in the future and dismiss those Veterans whose already stolen funds are in the past and are now of no concern. And on the stone alter of business, the line of Veterans moves forward to have his or her case examined; one or two minutes, then in off to the alter. Here is were the Veterans (whose plea still pending) beating heart is displayed to the Veteran and then to the pogie crowds. Blood of of another sacrifices by the VA, pushes business and them that much closer to one another. In fact some of that is already here

My name is Charles W. Reed III and during 2001 through 2008 I was performed VA loans for our brothers in Arms, and in 2004 I went to work for Wells Fargo Bank in the Omaha NE area and right outside of Offutt AFB I was working, and I discovered that this branch right outside the gate had not done a VA loan in over 2 years.

However at the smaller bank across the street and another location not far away, myself and another guy who at one time was in the Reserves and at one time a bank president. He and I probably performed more VA loans that any two people in the Country to together from 2002 to 2007.

When I first started for Wells Fargo I refused to sell Wells Fargo’s over price VA loan to our military families, until I got a concession to the pricing where they made an exception to the pricing and I cut my commission so that the pricing was at least the same as the market around us.

Next I had to fight with the underwriters who did not no how to properly underwrite the files and where disqualifying all the VA loans. I fought and had the Dept of VA underwriters out of Minneapolis talk with Wells Fargo’s staff underwriters to over turn the disapproved loans.

However what ended up happening with the other mortgage loan officers they would sell another product like a 80/20 (even if the loan was approved for VA loan) or refer the loan to one or two of the subprime divisions in MORE or Wells Fargo Financial that would sell a subprime adjustable mortgage loan.

Bottom-line is that Wells Fargo was steering military families into unsafe loans. I had called VA and reported the problem back in 2005, plus I wrote Warren Buffett who was and still is a major shareholder in the company and told him I needed help with a Provisional Patent I had submitted in May 2005 that would help the military families in receiving fair mortgage loan pricing and help in high cost areas housing cost issues. As you who guess Mr. (My secretary tax rate is higher than his) Buffett never answered my letter.

Now bringing things to today issues, we have a blatant violation of the law with Wells Fargo Bank illegally foreclosing on VA loans that Washington Mutual Bank (WaMu) placed into Ginnie Mae pools. What has taken place is that all WaMu government insured loans that where either originated (made) or purchase the loan from another, were placed under Wells Fargo’s servicing arm in an agreement that was signed Jul 31, 2006.

Starting in 2006 the 1.3 million government insured loans were now a part of Wells Fargo Bank’s servicing ONLY, as Wells Fargo did not purchase…

What else they don’t want to tell you is that Wells Fargo had stop even processing VA loan for the HAMP before the VA HAMP came into effective on Feb 1, 2010. Another thing is that Wells Fargo keep foreclosing on loans and did not even process the requests for the VA HAMP. Wells Fargo did not even have people trained to review the request until after Aug 8, 2010 before Wells Fargo VA HAMP was online.

What people were being told by Wells Fargo as they were trying to get answers about the modification was that they had to talk to the investor on the loan because you had a investor loan, but they could not tell you who the investor was. They played this game because Ginnie Mae held the blank Notes and could not change a interest rate or term by law, as they are not a lender and they did not have a financial interest in the mortgage loans.

The Dept of VA acted as if they lent military families the money for these home loan when in fact the VA is just a program and not a bank and they do provide insurance and the false insurance claims by Wells Fargo after the fraudulent foreclosures which those proceeds went to Ginnie Mae and Wells Fargo got to keep the False Claims that amounted to 10% of the loan balances.

Why do you think the FHA has a $16 billion shortfall? The FHA has a $70 billion loan lost which is 700,000 loans of the 800,000 loans that the OCC & Fed is saying that should have been modified, but actual the loan are free and clear of that debt and did not need a modification. So we know at less 50,000 military families were foreclosed in 2009-2010 of that 800,000 loan that should have been modified.

But the problem is larger than just those two years. I have the ability to recreate all the loan and tell the government exactly what took place with the military families, however the Dept of VA is still stuck on stupid as I have complained to them over 2 yrs ago. Here is who I am Charles W. Reed III Blackstarborn@yahoo.com

The VA Secretary is welcome to contact me if they would like to get back the billions that were stolen from that department in buying stolen properties and paying out fraudulent insurance claims. We talking about $5 billion in properties and $500 million in False Claims and the total with treble damages the VA is owed $16.5 billion. The VA is owed this money because Ginnie Mae is running a Ponzi scheme in having phony securities!

Bank of America announced it’s on track to fulfill consumer relief requirements as part of the national mortgage settlement within the first year of the three-year agreement.

So far, the bank has completed or approved $15.8 billion in consumer relief for about 164,000 homeowners as of September 30.

The bank is required to offer more than $7.6 billion in relief through first and second lien modifications and foreclosure avoidance solutions, but the credit is not given dollar-to-dollar. Thus, the actual gross amount of relief would be much higher than the actual amount credited, the bank explained during a conference call Wednesday.

One form of consumer relief offered through the settlement is first-lien principal forgiveness, which BofA has offered to 30,000 customers, leading to $4.75 billion in principal reductions.

On average, nearly $150,000 in principal balance is reduced through the program and monthly mortgage payments are lowered by about 35 percent.

During the call, Eric Telljohann, BofA SVP, revealed roughly 60 percent of the first-lien reductions were applied to investor portfolios, while 40 percent went to the bank’s own portfolio.

When determining who qualified for the principal reduction program, Telljohann says the bank took all borrowers who were eligible in the bank’s portfolio as of January 31, 2012, and added, “it was a matter of delegated authority from the investor.”

Since the borrowers who receive a principal reduction are delinquent and underwater, Telljohann explained the modifications are both good for the borrower and the investor.

“We always are evaluating to make sure we have a win-win…that both parties benefit,” Telljohann said, further stating it is BofA’s belief that “by providing this payment relief, we are preventing a foreclosure from happening.”

However, Chris Katopis, AMI’s executive director, views the settlement as being harmful to investors.

“Many of us expected a settlement to hold servicers responsible for their misconduct; not a bank bailout settling with other people’s money,” he said in an emailed statement.

In addition to principal reductions, the bank announced it has provided 62,000 borrowers with short sales or deeds-in-lieu of foreclosure.

Interest rate relief is another option offered by the bank. As of September 30, about 1,000 interest rate reductions have been completed. Rates are reduced to 4.25 percent and are offered at no cost for eligible borrowers who are current, but have a loan-to-value ratio above 80 percent.

In addition, the bank has offered…

Did I miss something? I didnt see a listing of these subject companies. I think we, as consumers, desreve to know WHICH companies are on this list of deceptive/dishonest mortgage lenders. Help us protect ourselves by giving us ALL OF THE INFORMATION. I’m getting ready to purchase a home and it would certainly be beneficial to know this.

The problem is that your information is public once you buy a home. Your veterans status, where you live and other information is available to anyone as long as they pay the local government entity either the city hall or county clerks office where you live and your information is fair game. This leaves the veterans as easy pray for theses snake oil salesmen. I would recommend you petition that your local elected officials to make it not legal for your address and name not be made so easy to obtain. I am not sure it will work but if you get enough people complaining about the issue then they will eventually get tired of recieving complaints and do something.

I use all unwanted solicitations as fuel for my fire…it keeps me warm in the winter.

WHY ARE’NT THESE CRIMINALS IN JAIL!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

NO ONE GOS TO JAIL IN AMERICA ! WHY??? BECAUSE THEY HAVE MONEY! AND THEY KNOW SOME ONE! WITH POWER! SO WHERE DOSE THAT LEAVE ME! A, DISABLE VETERAN ! THE LITTLE GUY WHO PUT HIS LIFE ON THE LINE FOR HIS COUNTRY ! AND WHAT DID I, GET FOR IT! KICK TO THE CURB! WHERE IS MY PRESIDENT , TO PROTECT MY VETERANS RIGHT’S!

They need to investigate company called Bankers Life and Causalty. These employees are targeting military people who get disability from government, VA, and once on MEDICARE they represent themselves to help you with long term care so your families wont have to take care of you. Well honestly my parents had the policy and I also got hooked on lies too. My dad passed but before he died we tried to get help thru long term care. Answer was: Medicare pays 80% And your tricare for life pays the balance of 20%. Gee it seems this company takes your money and never gives one dime back or give any help. Then when my Mom passed the same thing happened. Do not cancel your long term care with them until hopefully this dept will investigate and get a class action out there to stop them from this ungrateful tactic to seniors and military. Yo probably paying about 456.00 month for this policy. Buyer beware…..good luck…..you have been warned. They dont care about you just your money. Read fine print…your recieving goverment benefits of any kind they will sell you policy in fine print states government benefits must be use up total before they start paying on policy..

What is the best company to refinance with and what is the going interest rate?

Go with James B. Nutter Co. I have refinanced with them now (3) times and I am down to 3.5%. Never a closing cost. They are fast and honest. Love working with them. They are straight shooters. No hidden cost. Never paid a dime to refi.

There is a great leander called guild mortage out of colorado but workd many states. Ssk for joshua graham. He knows everything about s va no no. It codt us only 250.00 to get our home 4months ago and we got in program at navy fed that gave us 1000.00 back gor just using they real estate agent. And we got our losn throu ld guild morta gr not navy fed. Also guild mortage gsve us bsck the apprisal fee. This very true I livr in the house and we are both disabled and thats our only income and husband retirrmrnt. Other companies say they no a va no no but they don’t so go throuhh navy fed s real estste agents thay know.

I’m a Korean vet, so my home no longer has a mortgage on it. I’m looking for an HELOC (Home Equity Line Of Credit) to do interior improvements (kitchen, carpets, etc) and buy a new car. I’m looking to borrow up to 40% of the market value of the property. I can’t find any lenders that will do an HELOC. Anyone know of a lender who will. The property is in San Jose, CA.

Does anyone out there know of a gov program that will re-finance my severly upside down Florida condo? I no longer live in it – it’s rented – as I moved for employment/family reasons. I’m not late on payments as my retirement check is keeping it afloat but, I feel like it’s money down the drain at this point. I have about a $74,000 deficit between what I owe and what it’s currently worth. It seems because I can technically afford to keep throwing good money after bad that I don’t qualify for anything out there?

It would have been better if the VA just published the names of the companies that are misleading in their ads. I average on a weekly basis 5 letters tell me to refinance at a lower rate. One company uses a seal much like the VA seal. Another cites an interest rate that is not available when you call. Still another says this is your last chance to refinance, rates will go up. Finally, one comes that says Official VA Mortgage information as if the letter was coming from the VA. I say… if someone is trying to pull the wool over your eyes, then don’t do business with them… and let your veteran buddies know who they are so they don’t get shafted…. I’ve refinanced three times in the last 14 months.. I know what is real and what is misleading…

Did you refinance or did you streamline? There is a difference….

i’VE EXPERIENCED BOTH FROM LENDERS AND REALTORS ALIKE THAT THE

BAIT AND SWITCH TACTIC IS USED QUITE OFTEN, THEY OFFER A PROPERTY A AN AFFORDABLE PRICE, THEN WHEN YOU MAKE AN OFFER SUDDENLY THAT

PROPERTY NOT AVAILABLE. BUT THERE IS A PROPERTY IN A HIGHER PRICE

THAT YOU CAN QUALIFY FOR. HAPPEN QUITE OFTEN!

I applied to the Veterans Home Loan Network. I did not Qualify because my Home was not worth over $100,000. Tried a Couple others that stated in advertising the they Could get me a Loan. Same Denial also plus they offered to Lower my Interest rate on a Re Finance. My Home I purchased 3 1/2 years ago is worth less than the amount Financed by $15,000. Based on Tax Value. Not Home Value. Also told I was too Old & my income was not considered permanent due to My Retirement on Disability. I wondered if the VA was watching these Predatory Lenders with Large Closing costs. Thanks I hope all Veterans like me see this & Beware!

Age has nothing to do with qualifying for a va loan or for that matter any loan. Also with a VA rate reduction Loan (VARRL), the actual value of the home is not a consideration, appraisals are not required by va rules. In addition you can get refinancing at low rates and not pay any closing cost at all, I’ve done it twice and I am in the process of the third right now. All you have to do is a Google search and you can find many reliable lenders, just begging for a veterans business because VA loans are the surest thing going….

I was trying to refi with the same results then Navy Fed loan officer told me to call my lender and ask about the va irrl refi. Did this and BOA dropped me to 3.75 from 6.5 with minimal paperwork and no costs. What I owed when I went into closing was what I owed when I walked out. Payments dropped 600.00 a month almost, and although I am back to a 30 yr mortgage from 27 years remaining on the old one, if I pay what my old payment was (I am) and now the house is paid for in 17 years (total of 20 from original purchase). Saves me lots of interest, and if I need the extra money in a particular month, all I have to pay is what the new payment is.

Try talking to your lender…..

I would take heart most lending officers like you saw are as lazy as dog who won’t hunt.

I have heard of many ortgages written for customers, clients or people on disability.

I am a disabled combat vet that got a home loan w/VA compensation alone. Don’t receive SS nor any other income. So it is definitely possible w/in reasonable home value.

I am Larry D. Pinnix, my date of separation (DOS) from the USAF was

April 27 1988. At seperation i’ve been receiving approximately 5 – 10 per

percent compensation. I really need assistance in many areas that

i have’nt been able to obtain since being separated from the military.

Please furnish me what ever information you have available.

keep righiting the bastards,it took me, ten yrs to get 100o/o only because they said no the first three times, then i let the have it both barrels,and did not sugar coet the 5 page letter, but you do have docter’s recmendation,and other resorses,of som sort,or ask to see a shrink at a va mac and he gets you pissod off poke hin one.